")

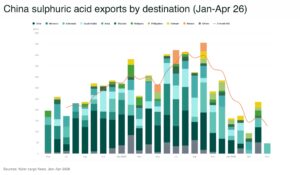

Uranium’s Cigar Lake shutdown exposes mining’s sulphuric acid crisis

On July 1, Cameco suspended mining at Cigar Lake, the world’s highest-grade uranium mine, after operational problems shut the sulphuric acid plant at Orano’s McClean

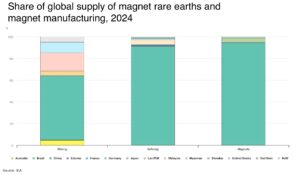

Rare earth elements are essential to permanent magnets used in electric vehicles, wind turbines, robotics, defence systems and advanced electronics.

Supply remains heavily concentrated with China controling around 60% of magnet rare earth mining, 91% of refining and 94% of permanent-magnet production.

Rare earth elements, or REEs, are a group of 17 chemically similar metallic elements used in permanent magnets, catalysts, electronics, lighting, medical technology and defence systems.

The group consists of the 15 lanthanides, plus scandium and yttrium:

Promethium is radioactive and has no significant natural commercial supply. Most rare-earth markets therefore focus on the other elements.

Despite their name, many rare earths are relatively abundant in the Earth’s crust. They are considered “rare” because they are seldom found in deposits that can be mined, processed and separated economically.

Today, rare earths support electric motors, wind turbines, smartphones, aircraft, catalysts, lasers, medical equipment and military systems. Their strategic importance comes from these specialised uses and the concentration of processing and magnet manufacturing in China.

Rare earths have unusual magnetic, optical, catalytic and electrochemical properties.

Different elements perform different functions:

Rare earths are not a single commodity. Each element has its own supply, demand, price and substitution dynamics.

Permanent magnets are the most strategically important and valuable rare-earth application.

Neodymium-iron-boron magnets, commonly called NdFeB magnets, are among the strongest permanent magnets commercially available.

Their high magnetic strength allows manufacturers to build motors and generators that are:

A typical NdFeB magnet contains neodymium and often praseodymium. Dysprosium or terbium may be added where the magnet must resist demagnetisation at higher temperatures.

Not every NdFeB magnet contains all four elements. Manufacturers adjust the composition according to performance, operating temperature, cost and supply availability.

Rare-earth magnets are used in many electric-vehicle traction motors.

Permanent-magnet synchronous motors can provide high efficiency, strong torque and compact size. These characteristics make them attractive for battery-electric and hybrid vehicles.

Rare-earth magnets may also be found in:

Not every electric vehicle uses a rare-earth permanent-magnet traction motor. Alternatives include induction motors, electrically excited synchronous motors and other magnet-free designs.

Vehicle manufacturers can therefore reduce rare-earth exposure through motor design, although alternatives may involve trade-offs in weight, efficiency, cost or manufacturing complexity.

Permanent-magnet generators are used in some wind turbines, particularly direct-drive and offshore systems.

These generators can reduce the number of moving parts and avoid the need for a conventional gearbox. This may improve reliability and reduce maintenance requirements in difficult offshore environments.

Not every wind turbine uses rare-earth magnets. Geared turbines and electrically excited generator designs can operate without them.

Rare-earth demand from wind power therefore depends on both installation growth and the market share of permanent-magnet generator technologies.

Robots and automated systems use compact electric motors to produce precise, controlled movement.

Rare-earth permanent magnets can improve the torque, efficiency and power density of motors used in:

The amount of rare-earth material required depends on the number, size and design of the motors.

Robotics could become an important demand source, but long-term requirements will depend on commercial adoption, engineering choices and improvements in magnet efficiency.

Rare earths are used across smartphones, computers, headphones, displays, hard-disk drives and communications equipment.

Applications include:

Data centres use rare-earth magnets in hard-disk drives, cooling systems, fans and power equipment. The effect of AI growth on rare-earth demand depends partly on the balance between magnetic hard-disk storage and semiconductor-based solid-state storage.

Rare earths support systems that require compact size, precision, heat resistance and dependable performance.

Applications include:

Samarium-cobalt magnets are particularly useful where high-temperature performance and corrosion resistance matter. NdFeB magnets are used where very high magnetic strength is the priority.

The quantities used in an individual system may be small, but substitution can be difficult without redesigning equipment or accepting lower performance.

Cerium and lanthanum are widely used in catalysts.

Cerium-containing materials help vehicle catalytic converters store and release oxygen, improving their ability to control exhaust emissions.

Lanthanum and other rare earths are used in fluid catalytic cracking, a petroleum-refining process that converts heavy hydrocarbons into petrol and other higher-value products.

Rare-earth catalysts are also used in chemical manufacturing and emissions-control systems.

Catalysts represent a large-volume rare-earth market, although the value per kilogram is generally lower than for magnet materials such as neodymium, dysprosium and terbium.

Rare-earth phosphors convert energy into specific colours of visible light.

Applications include:

Europium is associated with red and blue phosphors, while terbium is used for green. Yttrium commonly acts as a host material in phosphor systems.

Demand has changed as lighting and display technologies have evolved. The decline of fluorescent lighting reduced some established markets, while LEDs, lasers and specialised displays continue to use selected rare-earth materials.

Rare earths have several medical and scientific applications.

Gadolinium compounds are used as contrast agents in certain magnetic-resonance imaging procedures. Their use is medically regulated because free gadolinium ions can be toxic, so the element is administered in specially designed chemical complexes.

Other applications include:

Rare-earth magnets are also used in motors and sensors within medical devices.

Cerium oxide is widely used to polish glass, mirrors, display panels and precision optical surfaces.

Rare-earth compounds can also:

Applications range from consumer glass to optical equipment and semiconductor manufacturing.

Lanthanum, cerium, neodymium and praseodymium are used in metal alloys.

Nickel-metal hydride batteries use rare-earth-rich alloys in their negative electrodes. These batteries remain important in some hybrid vehicles, industrial systems and consumer products.

Scandium can be added to aluminium to create lightweight, strong and weldable alloys. Potential applications include aerospace, defence, sporting equipment and additive manufacturing.

Scandium supply and price have limited wider adoption, making its market distinct from the larger rare-earth industry.

Rare earths are often divided into light and heavy groups, although the precise boundary can vary between industry sources.

Light rare earths generally include elements such as:

They are typically more abundant and dominate many carbonatite and hard-rock deposits.

Heavy rare earths generally include elements such as:

They are often less abundant in conventional ores and can be more difficult to source economically.

Dysprosium and terbium are strategically important because of their role in high-performance magnets. Heavy rare-earth supply has historically depended strongly on ion-adsorption clay deposits in China and neighbouring supply chains.

Important rare-earth minerals and deposit types include:

Bastnäsite and monazite commonly contain a greater proportion of light rare earths. Xenotime and ion-adsorption deposits may contain higher proportions of yttrium and heavy rare earths.

The commercial value of a deposit depends on its distribution of individual elements, not simply its total rare-earth grade.

A deposit rich in cerium and lanthanum may have a very different value from one containing meaningful quantities of neodymium, praseodymium, dysprosium or terbium.

Producing a finished rare-earth magnet involves several distinct stages:

Each stage requires different technology and expertise.

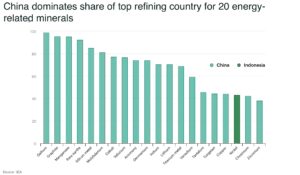

Because rare-earth elements have very similar chemical properties, separating them can require numerous solvent-extraction stages. A country may operate a rare-earth mine while remaining dependent on another country for separation, metal production or magnets.

China is the leading rare-earth mining country and holds a much stronger position in separation, refining, metal production and permanent-magnet manufacturing.

Other mining countries include the United States, Australia and Myanmar, while additional projects are being developed across Africa, Asia, Europe and the Americas.

Mining diversification has advanced faster than downstream diversification. The main strategic bottlenecks include:

A new mine does not create an independent supply chain unless its concentrate can be processed into individual oxides, metals, alloys and finished components.

Rare earths have become a prominent tool of industrial and trade policy.

China has imposed export controls and licensing requirements affecting selected rare-earth elements, magnets, processing technologies and dual-use products. The scope and implementation of these rules can change over time.

Restrictions can affect:

The durable market issue is not any single policy announcement. It is the ability of one country’s licensing decisions to influence industries that depend on a small quantity of highly specialised material.

Governments are responding through strategic inventories, public financing, allied-country partnerships and support for mining, separation, recycling and magnet manufacturing.

Myanmar has become an important source of feedstock for heavy rare earths, particularly material linked to ion-adsorption deposits.

Production can be affected by conflict, border controls, environmental enforcement and trade policy. Material may also enter downstream processing through China, making the supply chain difficult to assess using mine-production data alone.

This creates additional risk for dysprosium and terbium, which are used in high-temperature permanent magnets.

Rare-earth mining and processing can generate significant environmental impacts.

Potential issues include:

Monazite and some other rare-earth minerals can contain thorium or uranium. These elements must be separated and managed safely, increasing project complexity and cost.

Ion-adsorption clay mining may require less rock excavation, but poorly managed leaching can contaminate soil and water.

Environmental performance depends on deposit type, processing method, regulation, waste treatment and enforcement. “Low-impact” claims should therefore be evaluated at project level.

Rare earths can be recovered from permanent magnets, manufacturing scrap, batteries, lighting products and electronic waste.

Potential sources include:

Recycling remains challenging because rare earths are often present in small components embedded inside complex products.

Barriers include:

Magnet-to-magnet recycling can preserve more of a material’s value by recovering and reprocessing the magnet alloy directly. Chemical recycling separates the material back into individual rare-earth compounds.

Recycling can strengthen supply security, but it will take time for large volumes of EV and wind-turbine magnets to reach the end of their operating lives.

Manufacturers can reduce exposure to rare earths through material efficiency, substitution and product redesign.

Options include:

Substitutes may involve trade-offs in power density, weight, efficiency, operating temperature or system complexity.

For many applications, the practical question is not whether rare earths can be eliminated. It is whether they can be reduced without making the complete system larger, heavier, less efficient or more expensive.

There is no single rare-earth price.

Individual products trade separately, including:

Prices vary according to purity, form, location and contract terms.

Some deposits produce more low-value cerium and lanthanum than the market requires while producing relatively little high-value neodymium, dysprosium or terbium. This imbalance is sometimes called the rare-earth balance problem.

The economics of a project must therefore consider the full basket of elements and whether there is a market for each output.

The principal sources of rare-earth demand include:

Rare earths sit at the intersection of electrification, defence and industrial policy.

Key trends to watch include:

Rare earth elements are not one market but a family of specialised materials.

Their importance comes from the performance they enable in permanent magnets, catalysts, optics, electronics and defence systems. The strongest supply-chain risks are concentrated around magnet rare earths—particularly neodymium, praseodymium, dysprosium and terbium—and the processing stages needed to turn mined material into finished magnets.

For investors, manufacturers and policymakers, the central question is not simply where rare earths can be mined. It is whether those resources can be separated, refined and manufactured into qualified components at a competitive cost and acceptable environmental standard.

———————–

Rare earths are used in permanent magnets, electric motors, wind turbines, catalysts, electronics, displays, lasers, medical imaging, defence systems, glass polishing, batteries and specialist alloys.

There are 17 rare earth elements: the 15 lanthanides, plus scandium and yttrium.

Many are relatively abundant in the Earth’s crust. They are considered rare because economic concentrations are uncommon and the elements are difficult to separate from one another.

Neodymium and praseodymium are the principal rare earths in NdFeB magnets. Dysprosium and terbium may be added to improve high-temperature performance. Samarium is used in samarium-cobalt magnets.

No. Many use rare-earth permanent-magnet motors, but induction motors and electrically excited designs can operate without rare-earth magnets.

Rare earths are not major active materials in mainstream lithium-ion batteries. Their principal role in electric vehicles is usually in permanent-magnet motors and other components. They are used more directly in nickel-metal hydride batteries.

Yes. Rare earths can be recovered from magnets, batteries, lighting products and electronics. Recycling remains limited by collection, disassembly, separation costs and the relatively small quantities contained in many products.

China developed an integrated supply chain spanning mining, separation, metal and alloy production, magnet manufacturing and downstream products. Its advantage is therefore based on processing capacity, technical expertise and industrial scale as well as geological resources.

—

Reference sources for annual review: USGS rare-earth statistics, USGS Mineral Commodity Summary, IEA rare-earth analysis, USGS deposit overview and the US Department of Energy rare-earth overview.

On July 1, Cameco suspended mining at Cigar Lake, the world’s highest-grade uranium mine, after operational problems shut the sulphuric acid plant at Orano’s McClean

A new report by the London School of Economics warns that simultaneous buying by Australia, China, the EU, India, Japan, South Korea and the US

The US Army is will host critical minerals processing plants on military bases, leasing land to companies that can refine materials including lithium, graphite, boron

Within days of its IPO, SpaceX’s market value was pushing toward US$3 trillion, putting a public-market valuation on reusable rocket launches as the infrastructure layer

China has added MP Materials and USA Rare Earth to its export control list, restricting Chinese companies from supplying the two US rare earth firms

The G7 has agreed to reduce reliance on any single supplier of rare earths and permanent magnets to below 60% by 2030, in the clearest

Welcome to The Oregon Group, an investment research team focused on critical minerals, mining, energy and geopolitics.

Our independent capital markets experts are sharing their boardroom expertise and institutional experience to help you profit and hedge your investment exposure during this time of unmissable opportunity.