- US Trade Representative Jamieson Greer has urged allies to pay a “national security premium” for critical minerals sourced outside China

- US and EU are now assessing reference prices, border-adjusted price floors, price gap subsidies and offtake agreements

- US was 100% net import reliant for 12 critical mineral commodities in 2024, according to the USGS

The US is urging allies to pay more for critical minerals sourced outside China, in a direct challenge to the low-cost supply chains that have dominated global mining and processing for two decades.

US Trade Representative Jamieson Greer told the Financial Times that allies must be ready to pay a “national security premium” for minerals from trusted suppliers.

“When trading partners express concerns about the economic cost of price floors or mechanisms, I just say: what you’re talking about, which is cost efficiency, this is why we are in the situation we’re in,” Greer told the FT. “There is a premium we pay, and I call it the national security premium, and we will all pay a national security premium to have a secure supply chain.”

The message is blunt: cheap minerals helped build China’s dominance and higher-cost supply may now be needed to break it. Greer is developing proposals for allied trading partners, including Europe, to create price mechanisms that support non-China mineral supply chains.

Any premium would mark a major change in how critical minerals are priced with calls, not just to diversify, but to pay for diversification.

Subscribe for Investment Insights. Stay Ahead.

Investment market and industry insights delivered to you in real-time.

What is the critical minerals premium?

The latest plan says both sides will assess mechanisms including reference prices, border-adjusted price floors, standards-based markets, price gap subsidies and offtake agreements, focused first on selected critical minerals and supply chains, according to the official US-EU Critical Minerals Action Plan.

That matters because many Western projects fail at the same point: not geology, but economics.

New mines and processing plants need long-term price certainty. China’s scale, state support and processing dominance can make Western projects look uneconomic when judged only against spot prices.

Washington’s answer is to create a different market.

Why now?

The US was 100% net import reliant for 12 critical mineral commodities in 2024, while another 28 critical mineral commodities had import reliance above 50% of apparent consumption, according to the USGS.

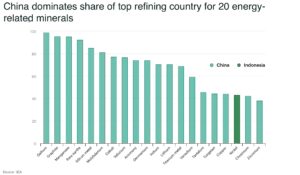

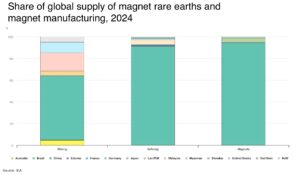

China remains central to this problem.

The USGS said the US imported at least 29 mineral commodities from China from 2020 to 2023, according to a USGS analysis of mineral import reliance.

For example, a major US defense prime conducted a recent, rare deep trace of its titanium supply chain, reaching 13 tiers down — it led directly to “Chinese mines, Chinese roads, and Chinese trucks” as confirmed by their supply chain specialists, according Stanford’s recent Critical Minerals and the Business of National Security report.

See our analysis on China’s titanium dominance: vertical supply chain, cost edge, and global ripple effects.

This is the policy gap Washington is trying to close. Critical minerals are needed for batteries, electric vehicles, grid equipment, semiconductors and defense systems. But many supply chains still run through China.

Can critical minerals become “free-range eggs”?

The Oregon Group raised the core problem in 2024: commodities are meant to be identical. A tonne of nickel is a tonne of nickel. A kilo of rare earth oxide is a kilo of rare earth oxide. That makes it hard to charge a premium based on where or how the material was produced.

But the same analysis argued that the market may still split. Just as consumers pay more for free-range eggs, Western buyers may need to pay more for critical minerals produced under higher environmental, labour and security standards.

The challenge is scale.

That is the gap the US is now trying to close.

No longer through consumer branding, but through policy.

What changes for prices?

The result of any official policy to pay a premium could be a more fragmented, birfucated global minerals market. One price may reflect the cheapest available material, often shaped by Chinese supply. Another may reflect verified, secure, non-China supply backed by allied buyers, offtake contracts, subsidies or price floors.

The US-EU action plan already points in that direction, with tools including price gap subsidies and offtake agreements.

Europe is also trying to build its own pricing infrastructure. EIT RawMaterials, an EU-funded agency, is working with Metalshub to develop a regional trading and pricing system for critical minerals such as rare earths, because weak price transparency has made it harder to finance new projects, according to Reuters.

The direction is clear. Governments want markets to price security, not just volume.

Conclusion

The premium will not be free.

Higher critical mineral prices could raise costs for battery makers, automakers, defense suppliers and grid equipment manufacturers. It could also create tension with allies if Washington is seen as shifting the cost of supply-chain security onto Europe and other partners.

There is also execution risk. Price floors can support new supply, but they can distort markets if they are too broad, too slow or too political. The question is whether governments can design a premium that funds real capacity rather than protecting uneconomic supply.

For now, the US is making the strategic choice explicit. If allies want critical minerals outside China, they may have to pay more for them.

Subscribe for Investment Insights. Stay Ahead.

Investment market and industry insights delivered to you in real-time.