- the Strait of Hormuz is not just an oil chokepoint. The Middle East accounts for about 24% of global sulphur production, and sulphur is the feedstock for sulphuric acid used across nickel, copper and fertilizer supply chains

- Indonesia, which produces more than 50% of global nickel, imports roughly 75% of its sulphur from the Middle East. Some HPAL plants hold only one to two months of sulphur inventory

- Sulphur prices were already around $500/t before the latest conflict and had risen another 10%-15% afterward

The Middle East accounted for around 24% of global sulphur production at 83.87 million metric tons last year; including 50% of seabourne trade of sulphur — which must be exported via the Strait of Hormuz.

Sulphur is essential to sulphuric acid which, in turn, is essential to processing critical minerals, including copper and nickel.

And, the sulphuric acid market was already tight before the latest Middle East disruption, increasing 500% before the latest conflict in Iran started.

Despite the oil price falling from highs on March 9, 2026 — after the US Treasury suggested using oil futures to suppress the price — the Sulphur price continues to rise, giving the game away and highlighted how, despite price suppression methods, prices rises will find their way through.

Why the Strait of Hormuz is a chokepoint for metals

Sulphuric acid is one of industry’s basic working chemicals. In mining it is used mainly in leaching, where ore is treated with acid so metals can be dissolved, separated and recovered. It is central to hydrometallurgy, especially for acid-intensive routes such as HPAL nickel, oxide copper leaching, and parts of the uranium, rare earths and titanium sulphate-route processing chains.

Without acid, a large share of low-grade or chemically difficult ore cannot be processed economically at scale.

Why does the Strait of Hormuz matter for sulphuric acid?

The short answer is that a significant percentage of global sulphur supply is produced in the Middle East, and the region’s exports depend on Hormuz. Argus reported on March 2 that sulphur cargoes were still loading at some Gulf ports, but with vessel backlogs outside Hormuz — reports the tanker transits through the Strait are down about 90% — show how severe the logistics shock has become. And, when ships stop moving through the chokepoint, replacement cargoes get more expensive and harder to source.

While the global economy focuses on the oil market, is the global metal supply chain also about to seize up?

What is at risk?

- sulphur exports from the Gulf

- sulphuric acid production and delivered acid costs

- HPAL nickel output in Indonesia

- acid-leach copper operations in Africa

- fertilizer buyers competing for the same feedstock

Acid is bulky, corrosive and not cheap to move over long distances, so this is not a market that can pivot instantly. New acid capacity cannot be switched on quickly, and alternative sulphur flows take time to redirect. That means price is likely to do the work first.

Which metals are exposed?

Nickel is on the front of the line

Indonesia has the clearest exposure to the tightening sulphur supply — the country now accounts for more than 60% of global nickel production — and imports around 75% of its sulphur from the Middle East.

Reports suggest some HPAL operators hold only one to two months of sulphur inventory, meaning a prolonged disruption could start to hit output quickly.

Nickel supply has often been framed as abundant because Indonesia has grown so quickly. But a meaningful slice of that growth depends on acid-intensive processing. This is the kind of bottleneck that does not show up cleanly in mine supply forecasts until it is already biting.

Copper and cobalt in Central Africa

Africa’s copper belt imports approx 2 million tons of sulphur a year, approx 90% of which originates from the Middle East, for oxide copper leaching.

The Democratic Republic of Congo (DRC) also accounts for roughly 70% of global mined cobalt supply — which also needs sulphuric acid.

“I have heard that traders are already struggling to source any. Sulphuric acid prices will therefore significantly increase across Africa… and if the disruption lasts longer than ~3 weeks, copper oxide operations will have to close as they’ve run out of acid” — Robert Friedland, Ivanhoe Mines, founder and Executive Co-Chairman

—

| Metal / sector | How sulphuric acid is used | Exposure to Hormuz‑linked sulphur |

| Nickel | HPAL and other laterite leach circuits are highly acid‑intensive, both for MHP and nickel sulfate production | Indonesia’s HPAL capacity is heavily reliant on Middle East sulphur imports and carries minimal inventory cover |

| Copper | Widely used in heap leaching, SX‑EW and other hydrometallurgical routes, especially for oxides and low‑grade ores | Central African copperbelt imports ~2 Mt/y sulphur from the Middle East; disruptions directly hit oxide leach capacity |

| Cobalt | Often co‑produced with copper and nickel in acid leach circuits | DRC supplies 70% of mined cobalt; reliance on imported sulphur links cobalt supply to Hormuz flows |

| Uranium | Sulphuric acid is a standard reagent in acid leaching and in‑situ recovery | Projects using acid ISR or leach, particularly where sulphur is imported, face rising reagent costs and potential curtailments |

| Rare earths | Used in acid cracking and leaching in several flowsheets | Projects outside China that rely on imported acid or sulphur are most exposed; Chinese operations are partly shielded by captive capacity |

| Lithium | Acid used in some leach‑based routes and in upstream reagents for conversion | China’s refining base is indirectly exposed via higher global sulphur and acid prices and any constraints on imports |

| Titanium dioxide | Sulphate process reacts ilmenite or slag with sulphuric acid | Pigment producers using the sulphate route face higher reagent costs; chloride‑route producers are less affected |

| Zinc, manganese, and others | Various hydrometallurgical flowsheets and secondary processing use sulphuric acid | Exposure is more asset‑specific; operations with captive acid are advantaged over toll buyers |

—

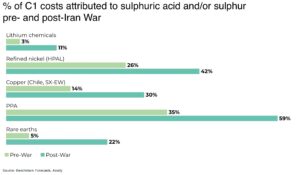

The big picture is that sulfuric acid is most important where metals are recovered by leaching rather than just smelting. That is why shortages hit nickel, copper, uranium and some rare earth projects especially hard.

However, not all metal processing operations are equally exposed, with some miners insulated for a variety of reasons, including:

- other exporter, for example, Australia, the world’s largest lithium spodumene producer, receives most of its sulphur from Canada, so should remain relatively insulated — but, that said, the second-largest supplier is Qatar

- sulphuric acid can also be produced as a byproduct of copper smelting (eg Ivanhoe’s Kamoa-Kakula complex has its own acid plant)

So, operations with captive acid plants or access to sulphur from smelter off-gases are better insulated. Operations that depend on imported sulphur are not.

And, importantly, suplhuric acid is no longer a side-product. In tight conditions, it can be a source of earnings strength for integrated players and a cost problem for everyone else — becoming itself a “critical mineral”.

Why is sulphuric acid important?

Sulfuric acid matters because it is one of industry’s basic working chemicals: a strong, highly corrosive acid with a powerful ability to break down minerals, strip impurities and drive chemical reactions.

In metals processing, it is used mainly in leaching, where crushed ore is treated with acid so valuable metals such as copper, nickel, cobalt and uranium can be dissolved and then separated, purified and recovered.

The process makes it central to hydrometallurgy and especially to acid-intensive routes such as heap leaching and HPAL processing of laterite nickel ores. It is usually made by burning sulfur to produce sulfur dioxide, oxidising that into sulfur trioxide, and then converting it into acid in a controlled process.

The reason it is so important is simple: without sulfuric acid, a large share of low-grade or chemically complex ore cannot be processed economically at scale.

Fertilizer too

Another pull on tightening supply is fertilizer. Any scramble for sulfuric acid supply by miners puts it up directly against the fertilizer industry — which accounts for 60% of global demand. That raises the stakes well beyond metals: sustained shortages would not just push up farm input costs, but risk cutting crop yields and worsening food insecurity.

Conclusion

The Strait of Hormuz disruption is not just an oil-market story. It is a metals-processing story (and food security story). A market that was already short sulphuric acid is now facing a fresh logistics shock at the same point where about a quarter of global sulphur production sits.

If you wanted to look for a single point of failure across such a broad range of metals produced — sulfuric acid would be that single point of failure.