- spot gold traded over US$5,000/oz thoughout February 2026, steady after reaching $5,400/oz in January

- central banks bought 863 tonnes in 2025, with demand historically elevated and geographically widespread

- gold has overtaken the Euro as the world’s second largest global reserve asset, with central banks holding more gold than US Treasuries for the first time since 1996

Gold at $10,000 in 2026 isn’t a bull case, it’s a break-glass price, the kind you only see when something in the financial system snaps.

Gold is still trading near US$5,000/oz, after surviving (for now) a near -10% one-day drawdown on January 30, the steepest since 1983. Despite the recent fall, the gold price is still approx 75% higher than it was at the same point last year.

Layer on top the war in the Middle East, oil whipsawing higher, and a bid for real assets as central banks buy size, currencies are being “managed” weaker, with the war pushing energy, inflation and policy risk to the front of the tape. A major pivot point for gold from $5,000 emerges.

There is every possibility gold has further to fall but, right now, it’s in a hold-and-see mode — and could well be forming a new base to climb higher. What is the price waiting for, and what happens to the price if something systemic fails, especially as the fallout of the energy crisis in the Middle East is yet to play out.

What would gold at $10,000 actually mean?

A $10,000 print in 2026 is not “gold doing what gold does”. It’s gold re-pricing the monetary system.

So, rather than the clickbait “Can gold go to $10,000”, the more useful framing we’d suggest is: what kind of macro regime forces a 100% move from US$5,000?

Two things typically do that:

- real yields collapse (or inflation runs hotter than nominal rates can keep up with), making cash and bonds value-destructive in real terms

- a credibility event (policy volatility, fiscal dominance, debt monetization fears, sanctions architecture expanding) that moves gold from “hedge” to “reserve asset” faster than supply can respond

Both paths run through the same choke points: US real yields and US dollar credibility.

And, for now, the setup is real: central banks are still buying, the dollar is still weak over the last 12 months, and real yields threaten to be the next domino, and then we have crypto volatility to add to the mix on the margins.

The official bid: central banks are still the marginal buyer

The headline: central bank buying cooled in 2025, but it held steady.

Full-year data shows central banks purchased 863t in 2025, the “upper end” of the World Gold Council’s expected range with purchases historically elevated and geographically widespread.

eg Poland added 102t in 2025 and pushed gold to 28% of reserves, nearing a 30% target

Even more important is the intent: 95% of central bankers expect global gold reserves to keep rising over the next year, as Yuan falls 20% from 2022, with 76% of central banks believe gold will make up a higher share of their reserves five years from now (vs. today).

Central banks have been net gold buyers 15 years in a row since the 2008 financial crisis, reversing the behavior of the 1990s and 2000s, when many central banks (especially in Western Europe) sold hundreds of tonnes per year.

Importantly, central banks don’t chase momentum; they help de-risk the system. So, when they buy consistently, they steady the price as a structural backstop.

Devaluation for both dollar and yuan — confidence loss can be fast

The value of total annual gold investment more than doubled in 2025 to reach US$240 billion, smashing the previous annual record of 1,805t, which has held since 2020.

The two biggest drivers: safe-haven and diversification from:

- currency (dollar and yuan) weakness

- geopolitical and geoeconomic risk

- and expectations of lower interest rates

We argue the most important is the moves in the dollar and yuan:

- share of US dollar holdings decreased slightly to 56.92% in 2025Q3, the lowest since 1995

- share of Chinese renminbi holdings decreased to 1.93% in 2025Q3

This is not currency collapse (as we’ve argued before, we’re not believers in the idea that the dollar is about to lose its place as the reserve currency — although events in the Middle East may have some very long-term consequences for currency markets if it goes very badly for the US intervention), but there is significant volatility: between April-June 2025, the dollar dropped 9% versus the euro, but in wild swings in the US$9.6 trillion—per-day foreign exchange market mean outsized impact on other assets at the margins.

“The value of the dollar is great,” US President Donald Trump said when asked if he thought it had declined too much on January 27. The dollar then hit a session low of 95.566, the lowest since February 2022.

Then there’s China’s “management” of the yuan.

The renminbi’s real effective exchange rate has fallen by nearly 20% since early 2022, increasing the appeal of gold as a store of value and contributing to upward pressure on prices.

eg in December 2025, Chinese state banks and PBOC bought up dollars to slow the yuan’s appreciation — up to US$120 billion — a “insane number”, according to Brad Setser on the Council of Foreign Relations.

When two of the biggest currency blocs are both incentivized to keep financial conditions loose, gold’s appeal as the non-liability reserve asset rises.

A weaker dollar isn’t, by itself, a $10k trigger. But if markets start to price fiscal dominance, and simultaneously start to believe China will tolerate periodic yuan weakness to offset trade shocks, gold can gap higher fast because the “safe” alternatives begin to look politically contingent in both directions.

And, the Iran conflict has raised the odds of exactly the kind of fiscal dominance and sanctions sprawl that push gold along the spectrum from “hedge” to “core reserve”. Each ratchet tighter – energy sanctions, reserve freezes, weaponised payment rails – nudges more actors to diversify into assets that sit outside the system.

Real yields: the headwind that needs to flip

Right now, real yields are not screaming “monetary breakdown.”

The 10-year inflation-indexed yield is approx 1.78% in early March 2026 — and, normally, a positive real yields raises the opportunity cost of holding gold, but 2025 suggests this can be overridden.

But the Iran war is precisely the kind of shock that can flip that headwind into a tailwind. War spending, higher energy prices and fragile growth all tug in the same direction: bigger fiscal deficits, more political pressure to avoid aggressive tightening, and a higher tolerance for “running the economy hot.”

For the gold price to hit US$10,000, one of two things probably need to happen:

- real yields fall hard, either because nominal yields drop on a growth scare and faster cuts, or because inflation expectations rise while interest rates lag

- inflation stays hotter than policy can neutralize, not “hyperinflation,” but persistent upside that keeps real returns on cash/bonds unattractive, especially if bond volatility rises and policymakers become more cautious about tightening into a funding problem

There are lots of ways this thesis can play out, for example:

Despite official inflation numbers, we suspect (as this Reuters report argues) that inflation was already higher than reported — and expectations certainly suggest higher core inflation. And now, most importantly, the energy price spikes in the fallout from the war in the Middle East will invariably push up inflation everywhere.

Uncertainty and financial constraints will be important.

For example, an expectation the US will lower rates just as inflation pushes Trump-backed Federal Reserve Chairman nominee, Kevin Warsh, to raise them. In a market already pricing “managed currency weakness” and higher policy volatility, that’s precisely the backdrop where real yields can become the next domino — and gold starts behaving less like a commodity hedge and more like a monetary asset.

Crypto rotation is not a meme anymore

Crypto doesn’t need to die for gold to win. People just need to not believe it’s a reliable safe-haven.

On February 11, 2026, Bitcoin fell to approx $66,000, a far cry from the US$124,000 in October 2025. And, the capital pivot out of speculative tech and crypto and into real assets is showing up in fund flows and equity performance. Mutual funds focused on gold mining firms are now 2025’s standout winners, overtaking even this year’s high-flying AI and tech funds.

For crypto enthusiasts, Bitcoin was supposed to be the new reserve asset, but so far, central banks are clearly choosing 8,000-year-old gold over 15-year-old crypto when the stakes are highest.

Hard assets backed by policy: “We’re not going to let a group of bureaucrats in Beijing manage global supply chains,” declared Treasure Secretary, Scott Bessent — so imagine what he really thinks of crypto currencies

Supply struggles to respond fast enough

Total gold demand in 2025, including OTC, exceeded 5,000t for the first time.

There is no gold deficit, with mine production hitting an estimated new record of 3,672t in 2025 (and recycling hitting 1,404t). However, global mine production has essentially plateaued over the past 5–7 years.

Many of the richest historical gold regions are in decline. For example South Africa’s Witwatersrand Basin, which alone has yielded an estimated 30-40% of all gold ever mined, saw annual output fall from a 1,000 ton peak in 1970 to just 157 tons in 2017. Likewise, other once-prolific gold belts – the Carlin Trend in Nevada and Australia’s Kalgoorlie “Super Pit” – are facing depleting reserves after decades of intensive mining — underscoring a looming supply cliff.

Meanwhile, a new gold mine takes 20.8 years on average from discovery to production.

And, without any new significant new mines, known gold reserves could run critically low within the next 20–25 years — a paradigm shift in gold market dynamics.

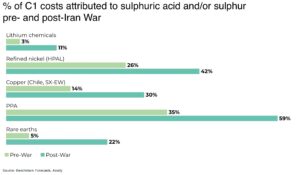

“If gold is being re-rated as a monetary reserve asset (not just a hedge), the market starts paying up for one thing the system can’t print: new ounces. That’s where juniors matter. They’re the exploration pipeline that can still deliver district-scale discoveries and future mine inventory, exactly what majors need when reserve replacement tightens.

Amex Exploration is positioning itself as that kind of “inventory builder.” The company’s Perron and Perron West land package in Québec has already attracted strategic capital as Eldorado’s investment significantly strengthens our exploration budget and reaffirms the high-quality potential of the Perron project and the recently acquired Perron West project. A defined resource and strong economics is only the starting point given the substantial untapped upside across the broader property”

— Victor Cantore, CEO and Director, AMEX Exploration Inc. (TSXV: AMX),+ President and founder of Bay Capital Markets

So, is the price of gold hitting $10,000 realistic?

Some estimates suggest gold could even hit US$30,000 in the years to come. We’re not there yet,but the current mix of war, energy shocks, fiscal strain and official gold buying means the upper tail on the distribution is getting fatter. If something breaks, gold could snap much, much higher.

The case for US$6,000–$7,000

- continued weakening of the US dollar (higher deficits and war spending)

- continued central bank buying (even if slower)

- ETF inflows stabilize, and safe-haven demand remains

The case for US$7,500–$9,000

- real yields to fall fast (growth scare + faster easing)

- perceived constraint on Fed independence or inflation control

- broader and deeper “reserve asset” demand from institutions that missed the first move

The case for $10,000+

- an explicit, extreme policy push toward sustained US dollar weakness (to manage debt and war costs)

- a genuine loss of confidence in the Fed’s ability – or freedom – to anchor inflation expectations

- a renewed round of commodity/energy inflation feeding into negative real rates, aka the debasement trade

In other words, the argument for a much higher gold price is fundamentally a monetary reset argument rather than a commodity-cycle argument.

Conclusion: $10,000 is a regime call, not a target

Gold doesn’t need $10,000 in 2026 to validate the thesis. At ~$5,000 today, it has already forced a new debate about money, reserves, and risk ,documented daily in price action and in official-sector behavior.

Importantly, with the latest geopolitical volatility in the Middle East and the rising oil price putting pressure on financial markets across the world, the thesis can play out in any number of ways; eg a renewed flight to safety into the US dollar and Treasuries, or a policy mix that keeps real yields decisively positive, would most likely have the opposite impact on the price of gold with a very sharp swing to the downside.

$10,000 is the “something breaks” number. And it certainly “feels” out there that something is close to breaking. Gold will rise because markets conclude the US is choosing a weaker dollar and lower real rates — by necessity, not preference. And the Iran war makes it easier to tell a coherent story for how we get there: pressure on real yields, pressure on the dollar, and a world that is gradually, then suddenly, more comfortable holding a bigger share of its wealth in an asset the system can’t print.

If markets come to believe that the only way to finance war and existing debts is through lower real rates and a structurally weaker dollar, gold above US$10,000 very quickly stops looking like a fantasy.