Sherritt International has suspended direct participation in its Cuban joint ventures, effective immediately, after new US sanctions targeting Cuba materially changed the company’s ability to operate on the island. The Canadian miner is repatriating expatriate employees from Cuba and has asked its Cuban partners to repatriate personnel from Canada.

The move is another shock to nickel cobalt supply chains, especially to the West.

Sherritt’s Moa joint venture in Cuba mines and processes nickel and cobalt, with feed then refined at the company’s Fort Saskatchewan refinery in Alberta. Sherritt says there is no immediate impact on the Canadian refinery, which will continue producing finished nickel and cobalt for sale, but its available feed inventory is expected to last only until about mid-June.

That creates the market question now being underpriced: what happens after June, especially as the strain is wider than Cuba with nickel supply was already tightening before Sherritt’s exit:

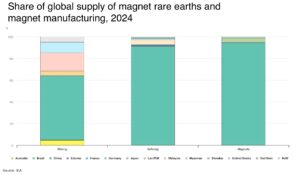

- Indonesia cutting 2026 ore mining permits to 250–260 million wet tonnes from 379 million tonnes in 2025. Indonesia now accounts for roughly 65% of global nickel supply, which means any disruption there moves the whole market. That risk is now spreading through the inputs chain

- Indonesian nickel processors rely on the Middle East for about 75% of their sulphur, used to make sulphuric acid for HPAL processing

- Australian miners have also been hit by diesel shortages and higher fuel costs as global oil-product flows are disrupted. Australia imports 84% of its petroleum products, with diesel stockpiles falling to about 30 days, forcing some smaller mining operations to scale back

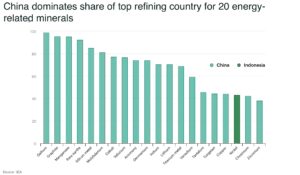

If Cuban partners cannot operate Moa reliably, the mine may have to remain curtailed or shut. If Cuba can operate the mine but can no longer rely on Canadian processing, it needs another route for material. That may open the door for China, already dominant in Indonesia’s nickel buildout, to take a larger role in Cuban nickel supply.

Sherritt has not been formally designated under the US executive order, but said such a designation “could occur at any time.” The company also warned the order may lead financial or service providers to stop supporting Sherritt’s operations or other business activities.

The timing matters. Moa was already fragile. In February, Sherritt said it would pause mining and processing in Cuba because of fuel supply constraints, after receiving notice that scheduled fuel deliveries to Moa would not be made.

The mine has also operated inside a deteriorating Cuban energy and labour environment. Sherritt previously cut 2025 guidance, citing lower-than-expected mixed sulphide production from Moa, while outside reporting has pointed to skilled labour shortages and blackouts as recurring operating pressures.

For Cuba, the blow is economic. Sherritt is one of the island’s most important foreign investors, while nickel and cobalt remain among Cuba’s key hard-currency export sectors.

For the nickel market, the bigger message is supply-chain risk.

This is not a demand story. It is a control story. A Western-linked nickel-cobalt chain running from Cuba to Canada has been interrupted by sanctions, fuel shortages and operating risk. That makes alternative sources of non-Chinese nickel more important, from Canadian sulphide projects to potential deep-sea supply from companies such as TMC.

If Moa shuts, supply tightens. If China steps in, control consolidates. Either way, Sherritt’s Cuba exit is bigger than one company. It is another warning that critical mineral supply chains can break quickly, and markets do not always price the break before it happens.