BHP has proposed a US$39 billion takeover of Anglo American, in what would have been the largest mining deal on record and create the world’s largest copper producer. Anglo America has rejected the offer, but we suspect this may just be the start, with reports Glencore is also considering a bid.

It’s a big deal, and part of a bigger trend.

Merger and acquisitions (M&A) across the mining industry were valued at US$121 billion in 2023, up 75% on 2022, according to GlobalData. Fitch’s BMI Research expects this “surge” to continue into 2024.

The deals that are attracting some of most attention for M&As across the industry are in the critical battery minerals sector, in particular, copper.

Some of the recent M&A examples include:

- BHP’s US$6.4 billion acquisition of OZ Minerals in May 2023, strengthening the group’s copper and nickel portfolio

- Newmont’s US$16.8 billion acqusition of Newcrest Mining, creating the world’s leading gold mining company, with significant copper production

- Rio Tinto’s acquisition of Turquoise Hill Resources in Mongolia for US$3.1 billion, boosting its copper portfolio

- the US$638 million merger between Reunion Gold and G Mining Ventures Corps in 2024

- Australian miner MMG’s acquisition of Botswana’s Khoemacau copper mine, a deal valued at US$1.8 billion

- the US$10.6 billion merger between US Livent and Australia’s Allkem to create a lithium mining giant

Is now the right time?

It’s no secret that the mining sector got burned with their proposed M&As in the early 2000’s, just as China’s housing mineral supercycle was starting to wind down, depressing the M&A market for a decade.

So, is this time any different, especially with high interest rates and inflation creating higher costs for miners.

Each company will have their own specific reasons for any merger or acquisition — most obviously profitability and consolidation to access new resources through diversity of assets — but the big factors driving the surging interest in potential M&As across the sector include:

- increasing critical metal deficits in global stockpiles

- geopolitics breaking supply chains, especially between the US and China

- demand to build out the energy transition to meet net-zero targets

- the difficulty in developing and permitting new mines, with the average time to build new mines in 2020-23 increasing to 17.9 years — almost 18 years — up from 12.7 years for projects started 15 years ago

- and, as per our latest report, to meet the massive energy demands forecast from artificial intelligence data centers coming online

A survey by White & Case, with 240 senior decision-makers across the industry (their largest ever set of respondents), found 47% of respondents thought the battery minerals sector the most likely to experience consolidation in 2024.

And deals often lead to more deals, as companies start to vie for advantage over competitors.

“It’s a lot cheaper to buy projects… First of all, the scarcity of projects that are shovel-ready and are…in quality jurisdictions are at a record lows. It’s been a dramatic under-investment in mining and development in the last 10 to 15 years. You’ve also seen projects that have been built, but most of them have gone wildly over budget, so the cost to build these projects are increasing by the month, by the year, so it’s a lot cheaper to buy projects that are almost completely built”

— Michael Gentile, co-founder of Bastion Asset Management, told Kitco News

“Looking into the coming years, we expect industry players to focus on transition metals as the need to reposition portfolios grows in response to the green energy transition… We expect to see demand for critical minerals surge, with a number of key markets at risk of going into deficit in the long term. The growing threat of supply deficits is acting as an incentive for miners to increase the share of critical mineral projects in their asset portfolio”

— Metals And Mining M&A: Strong Activity Set To Remain Over 2024, BMI Research

What about the critical minerals?

So, companies see opportunity and profit — but, will mergers and acquisitions improve the supply of critical minerals needed to meet net-zero commitments and the explosions in artificial intelligence demand.

In theory, larger companies and rising prices, mean more capital and efficiencies to bring on new supply. And, as highlighted by Ernest & Young’s latest annual report, access to capital is now the second most important concern among mining executives, up six positions from 2022.

We have four main concerns:

- will the larger companies, who have just finalized costly M&As, prioritize supply or profits?

- if companies are merging or buying up competitors ahead of an expected price surge (or, as ever, a possible fall in prices due to economic volatility), there is less immediate incentive to ramp up supply quickly

- M&As take time, sometimes years and are not always successful, which means capacity and capital that could be starting new mines (that take nearly 18 years to build) is not being started

- and, are the scale of the recent M&As big enough?

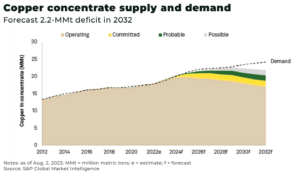

We’ve adjusted the chart below to highlight how long it will take for a new copper mine to come online if it’s started in 2024 — as far out as 2042 — and that’s if it’s started this year, which is increasingly unlikely if the companies are negotiating M&As, which will likely be completed just as the deficit starts to make an impact.

Small caps

The scale of the challenge is enormous. M&As are the obvious first step for projects in need of capital, but despite even the scale of proposals such as BHP’s US$39.9 billion bid for Anglo America — the recent rise in M&As may still not yet be enough.

“Over the past four years, there has been persistent talk of mergers and acquisitions and the necessity for industry consolidation. However, we have yet to witness this consolidation on the scale that has been discussed… It’s possible that 2024 will finally bring about the realization of these expectations”

— Theo Yameogo, EY Canada’s mining head, told the Financial Post

The UN Trade and Development (UNCTAD) has identified 110 new mining projects worldwide, valued at US$39 billion, with US$22 billion invested in 60 projects in developing countries. But UNCTAD warns that, to meet 2030 net-zero targets, 80 new copper mines, 70 new lithium and nickel mines each, and 30 new cobalt mines are needed.

To take lithium as an example, demand is forecast to rise by over 1,500%.

To meet this demand will need more exploration and mine development, which is where the small cap projects come in. Look away from the headline grabbing deals, and it is the small caps where the majority of M&As will take place, particularly after explorers need funding.

Analysis of capital cost announcements of over US$1 billion from 2020-2023 reveals the potential of capital investment in greenfield battery metal projects, with 75% of these projects at pre-feasibility or feasibility stage when final decisions will need to be made.

Conclusion

The recent increase in mergers and acquisitions across the mining sector highlight how the companies are preparing for potential soaring demand and deficits.

It’s a strategic move for the industry to unlock capital and profits, yet also serves as a cautionary signal that many companies are taking heed of forecasts predicting a critical minerals supply crisis.

Any mergers or acquisitions will be too late to stop any supply deficit in the short or even medium-term if demand continues to rise, driven by AI and net-zero targets.

But it means the industry is getting ready.