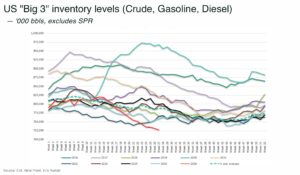

World oil demand is forecast to contract and not meet global demand in 2026, the IEA warns in its May 2026 monthly report. The warning comes as global observed oil inventories were drawn down by 250 million barrels over March and April, or roughly 4 million barrels a day.

The market is increasing set up for further “price spikes” ahead of peak summer demand.

The warning comes as the US Strategic Petroleum Reserve recorded its largest ever weekly release. The SPR released more than 1.22 million barrels a day last week, equal to about 8.6 million barrels over the week — surpassing the peak weekly draw seen in 2022 after Russia invaded Ukraine.

The oil market remains in deficit until the final quarter of the year, even assuming flows through the Strait of Hormuz gradually resume from the third quarter. “With global oil inventories already drawing at a record clip, further price volatility appears likely ahead of the peak summer demand period,” the agency said.

The scale of the supply shock is historic across oil, and — as we’ve reported — diesel and sulphuric acid, creating further shocks across the mining industry as the pressure is also moving from crude into refined products.

The IEA expects refinery crude throughputs to plunge by 4.5 million barrels a day in the second quarter to 78.7 million barrels a day, with margins supported by record middle-distillate cracks. That matters for miners because the industry does not consume oil benchmarks. It consumes diesel, fuel oil, lubricants, explosives, freight and power.

For mining, the risk is no longer abstract.

Diesel moves ore and waste rock. It powers haul trucks, drill rigs, generators, pumps, ships, rail and site logistics. It also feeds into explosives, reagents, contractor costs and shipping rates. When oil inventories fall this fast, miners face higher costs across the operating stack.

The most exposed operations are open-pit mines, remote projects, off-grid sites and bulk commodity producers with long transport chains. That includes iron ore in Australia, copper in Latin America, gold in Africa, uranium in Canada and critical minerals projects where infrastructure is already thin.

Higher diesel prices can raise cut-off grades, pressure strip ratios and make marginal tonnes uneconomic. Higher freight costs raise the delivered price of reagents, equipment and spare parts. Higher refinery margins hit diesel and fuel oil directly.

That creates a problem for the critical minerals build-out.

Many of the projects governments want most, from copper, nickel, rare earths, lithium, graphite and uranium, are fuel-intensive before they are electrified. They need roads, trucks, camps, generators, drilling fleets and shipping capacity.

A sustained oil shock raises the cost of bringing those tonnes to market just as the West is trying to accelerate supply.