Freeport Indonesia has pushed the full restart of the Grasberg Block Cave copper mine into early 2028 — an estimated 3% of global copper supply — extending one of the biggest supply shocks in the global copper market just as shortages of sulphur and sulphuric acid are threatening output elsewhere.

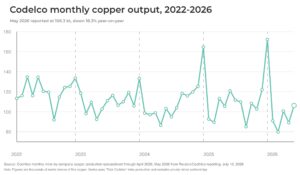

The delay matters because Grasberg is no marginal asset. The Indonesian mine produced about 1.5 billion pounds of copper in 2023, or roughly 680,000 tonnes, equal to around 3% of global mined supply.

Freeport had previously expected a faster recovery from the September mudflow incident, but the company now says wetter-than-expected conditions, groundwater issues and damage to ore-handling systems have slowed the restart. Production in undamaged areas has resumed, but only at around 40–50% of capacity as of April 2026.

That removes flexibility from a market already running with little spare capacity. The International Copper Study Group recently cut its 2026 mine supply growth forecast to 1.6%, down from 2.3%, citing constraints in the DRC, Chile and Indonesia, including Grasberg and Kamoa.

The timing is awkward. Copper demand is being pulled higher by grid upgrades, electrification, defence spending and data centres, while mine supply growth is slowing. Global mined copper output rose just 0.9% in 2025, according to Reuters commentary on the ICSG data, despite stronger long-term demand signals.

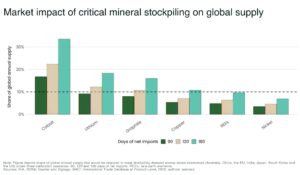

The sulphur problem adds another pressure point. Sulphur and sulphuric acid are critical inputs for solvent extraction and electrowinning, a process Goldman Sachs estimates accounts for about 17% of global copper supply. China’s move to restrict sulphuric acid exports from May, combined with disruption to Middle East sulphur flows, has raised the risk of further curtailments in copper-producing regions such as Chile and the DRC.

For investors, the signal is clear: copper’s supply problem is no longer just about long permitting timelines and underinvestment. It is now about operational fragility at tier-one mines, input shortages, geopolitics and infrastructure risk.

Consensus forecasts still vary. Goldman recently maintained a 2026 copper surplus forecast, while other analysts including JP Morgan have warned of deficits as supply disruptions cut into inventories.

But Grasberg shifts the risk to the upside. If one mine representing roughly 3% of global supply cannot return to full production until 2028, and sulphur constraints begin forcing cuts elsewhere, a 3–4% deficit may prove conservative. A 5–6% shortfall is no longer an extreme case. It is the scenario copper bulls will now be watching.