Spending on US data-center construction has overtaken conventional office building, with the latest US Census Bureau data showing private data-center construction reached a seasonally adjusted annual rate of US$50.706 billion in April 2026, up 28.1% year-on-year.

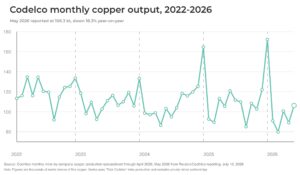

For mining and critical minerals, that makes AI less a software story than a fast-growing demand shock for copper, aluminium, gallium, rare earths, backup batteries and the grid equipment needed to power the buildout.

And, importantly, the US Census data defines data centers as buildings that contain hardware for storing, processing and transmitting digital information, while excluding racks or servers as equipment. So the latest figures captures construction put in place, but not the full mineral footprint of chips, servers and IT hardware that is increasing demand.

The US already has more than 3,000 operating data centers and more than 1,500 in development, according to Pew Research Center’s April 2026 analysis. Each project requires high-voltage connections, transformers, switchgear, backup batteries, cooling systems and miles of cabling before a single AI chip starts earning revenue.

The IEA estimates global demand for critical minerals from data center development is set to rise significantly by 2030, compared to 2024 levels:

- 2% for copper

- 2% for silicon

- 3% for rare earths

- 11% for gallium

The problem is supply concentration, with nearly 60% of refined copper, around 90% of aluminium and more than 90% of silicon, magnet rare earths and gallium came from the top three producing countries in 2024.

Our report on how the explosion of Artificial Intelligence (AI) is expected to spark a 10-year critical mineral supercycle as the massive energy needs of new AI data centers will increase pressure on global supply chains already under strain to meet global net-zero targets: