Guest post by Brian Paes-Braga, Founder, Chairman and CEO, The Metals Royalty Company (NASDAQ: TMCR)

Mr. Brian Paes-Braga is a Canadian-born entrepreneur and merchant banking executive. He was the Founder and CEO of Lithium X Energy, which in a period of 2.5 years, raised over C$50 million and was acquired in an all-cash deal for C$265 million. Since founding Lithium X in 2015, Mr. Paes-Braga has led company-building transactions across a range of sectors, with over C$5 billion in debt and equity financings into growth-oriented businesses. He was a board member of DeepGreen Metals, now TMC the metals company Inc., prior to its go-public transaction on the NASDAQ in September 2021.

The View from the Ground

I have spent the majority of my professional career, and the last 17 years of my life, in and around the natural resource sector, predominantly in mining. Growing up in Vancouver, and in Canada more broadly, instills an infectious energy for building value in this dynamic industry.

After the first 10-year sprint of my career, I had the opportunity to reflect on what I had learned. A few patterns began to emerge.

Most of my work took me to mines across Africa and South America. Investor meetings were largely in Australia, Canada, and parts of Europe and the UK. Strategic buyers were usually in Asia. What I didn’t take the time to consider then was why the United States, the most competitive country and largest economy in the world, was largely absent from that map.

Through a U.S. lens, the pattern becomes clearer: foreign assets paired with foreign investors. U.S. capital, meanwhile, flowed into technology, services, real estate, passive index funds, and the Shale Boom that made America the world’s largest oil producer.

That began to shift when Washington policymakers recognized how vulnerable the United States had become to China and other countries in securing the minerals required for daily life and to remain the dominant global power that it is today. And this extends far beyond the latest smartphone; it touches nearly every aspect of modern society.

Iron ore for steel and infrastructure. Nickel and manganese for specialized materials in defense applications. Rare earths for semiconductors. Copper for the trillions of dollars being deployed into AI infrastructure and the power grid. Uranium for reliable, long-life power. Lithium for batteries. The list goes on. In many ways, we in the West have forgotten a simple truth: the very foundation of civilizations throughout human history have been either extracted (mining) or grown (farming).

Returning as a Founder and CEO was a deeply intentional decision. If I was going to do it again, it needed to be for something meaningful, something vital to the world. Just as importantly, it had to be with people I trust and respect, who I’m proud to go to battle with every day. Together, we are committed to maintaining a culture of excellence and continuing our track record of building value for all stakeholders. That is the foundation behind the launch of The Metals Royalty Company (NASDAQ: TMCR). Welcome aboard.

How We Got Here: The Great Offshoring of Strategic Industries

For most of the twentieth century, the United States was the dominant force in global industry. In 1950, America produced 47 percent of the world’s steel. The industrial belt from Pittsburgh to Detroit to Chicago was not a regional economy. It was the engine of the global economy.

Starting in the 1990s and accelerating sharply after China joined the World Trade Organization in December 2001, the United States made a series of choices that seemed rational at the time. It exported its “dirty” industries, smelting, refining, chemical processing, under the banner of free trade and environmental responsibility. The logic was straightforward: let other countries handle the messy work while America focused on technology, services, and financial engineering.

Between 2001 and 2010, the growing U.S.-China trade deficit eliminated or displaced 2.8 million American jobs. 1.9 million of them were in manufacturing, nearly half of all U.S. manufacturing jobs lost in that decade. Entire communities built around steel mills, smelters, and refineries lost their economic base. The industrial heartland became the Rust Belt.

China absorbed those industries. Then it invested in them for two decades and built proprietary processing technology the West no longer has.

While the United States accumulated Treasuries as the world’s reserve asset, China pursued a different strategy. It systematically exchanged dollars for physical commodity control: mines, ports, processing plants, and off-take agreements across Africa, South America, Southeast Asia, and the Middle East.

The results are measurable. According to the International Energy Agency’s 2025 Global Critical Minerals Outlook, China is the dominant processor of 19 out of 20 energy-related critical minerals, with an average market share of roughly 70 percent. For some, the concentration is near-total: 98 percent of primary gallium, over 90 percent of battery-grade graphite, and around 60 percent of the world’s lithium and cobalt refining.

These Metals Are Already in Your Pocket, Your Car, and Your Country’s Arsenal

Everything in this world is either mined or grown. There are no exceptions. Every object you touch, every piece of infrastructure you depend on, every system that keeps a modern economy running traces back to something that came out of the earth or was cultivated from it.

The device in your hand. It looks simple, but it is anything but. A modern smartphone depends on more than 50 different elements, from lithium and cobalt in the battery to rare earths in the speakers and tantalum in the circuitry. These materials come from entirely different parts of the world and move through complex supply chains before ending up in a single device you use every day.

")

The car in your driveway. A conventional internal combustion vehicle uses roughly 35 kilograms of critical minerals. An electric vehicle like Tesla models uses approximately 200 kilograms. That is six times more. The battery alone requires lithium, cobalt, nickel, manganese, and graphite, each sourced, processed, and refined through supply chains that run through China.

Electric vehicle batteries require significantly more cobalt than consumer electronics. Global cobalt supply is overwhelmingly controlled by one country, the Democratic Republic of Congo, with China controlling the downstream processing.

")

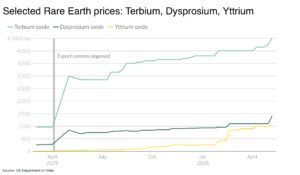

The weapons keeping you safe. An F-35 fighter jet requires approximately 900 pounds of rare earth materials. Precision-guided systems like Tomahawk cruise missiles use rare earth elements, especially in the magnets that power their navigation and control systems. In 2025, the U.S. was fully dependent on imports for 16 nonfuel minerals, and more than 50% reliant on imports for another 50.

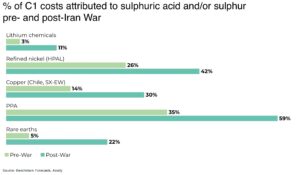

Even today, warfare remains fundamentally constrained by materials. In the first 96 hours of Operation Epic Fury against Iran, the U.S.-led coalition expended over 5,000 munitions across 35 weapons types. More than 850 Tomahawk cruise missiles were fired in the first four weeks alone, roughly nine times what the Pentagon buys in an average year. According to the Foreign Policy Research Institute, replacing the munitions fired in just those first 96 hours requires approximately 92 tonnes of copper, 137 kilograms of neodymium, 18 kilograms of gallium, and 37 kilograms of tantalum. China controls the global gallium production and neodymium processing. America builds the most advanced defense systems in the world on a supply chain it has progressively allowed to slip out of its control.

Data centers, power networks, and electrical equipment all rely heavily on copper for wiring, transformers, and circuit systems. Large data centers require significant amounts of copper. A typical facility can use between 5,000 and 15,000 tonnes, while hyperscale AI data centers can require up to 50,000 tonnes depending on size. Wind turbines, solar panels, and transmission infrastructure also depend on copper, nickel, and rare earth magnets.

The clean energy transition and the AI buildout draw on the same constrained supply of copper, nickel, and rare earth magnets simultaneously. The instinct of an American policymaker, faced with a supply problem of this scale, is to reach for the playbook that worked the last time.

This Is Not “Drill Baby Drill”: Why Metals Are Harder Than Oil

Americans have faced a resource crisis before. In October 1973, the Arab members of OPEC imposed an oil embargo against the United States. Within months, the price of crude nearly quadrupled to $11.65 by January 1974. Lineups for gasoline stretched for blocks. The economy went into recession.

The policy response was massive. On November 7, 1973, President Nixon announced Project Independence, with the goal of making America energy self-sufficient by 1980. Congress created the Strategic Petroleum Reserve in December 1975. The government and private sector poured billions into oil shale projects in Colorado and Utah. It took time, but America eventually solved it. When engineers successfully combined hydraulic fracturing with long-range horizontal drilling, the U.S. Shale Boom officially began, and U.S. shale producers could respond to price signals within 6 to 18 months. They drilled more wells, fractured more rock, and flooded the market with supply. By 2019, the United States was the world’s largest oil producer and a net exporter.

That playbook does not work for critical minerals. Shale is a repeatable, modular, fast-cycle business. Mining is not. And unlike oil in the 1970s, there is no cartel (OPEC) to negotiate with. China’s dominance of mineral processing is not a political position that can be reversed at a summit. It is three decades of industrial investment that has to be rebuilt from scratch.

According to S&P Global’s analysis of 127 mines worldwide, the average time from discovery to commercial production is 15.7 years. For mines that entered production between 2020 and 2023, the average climbed to 17.9 years. In the United States, the average is 29 years, the second longest of any major mining jurisdiction in the world, behind only Zambia at 34 years.

Consider Tesla’s lithium refinery in Robstown, Texas, one of the most ambitious private-sector attempts to bring refining capacity onshore. Tesla broke ground in 2023. With more than a billion dollars of investment, the facility did not begin producing lithium until late 2025 into 2026. That is the best-case scenario for a single refinery. Now multiply that across the dozens of mines and processing plants the country needs.

AI infrastructure, grid expansion, defense rearming, and the EV transition are all pulling from the same finite pool of materials at the same time.

")

What America Is Trying to Do: The Policy Response and Why It Will Not Close the Gap

The United States is now attempting the largest reversal of industrial policy in a generation. After 30 years of scaling back minerals investment, government agencies are no longer just diagnosing the problem. They are writing checks.

In February 2026, the State Department hosted a Critical Minerals Ministerial in Washington, the largest gathering of its kind in a generation. Secretary Rubio and Vice President Vance convened representatives from 54 countries plus the European Commission. The event launched FORGE, the Forum on Resource Geostrategic Engagement, and produced 11 new bilateral critical minerals agreements.

On the capital side, multiple agencies are moving at once.

The Department of Energy is offering project finance at or below Treasury rates for domestic mining and processing, with billions announced across critical mineral supply chains.

The Department of Defense is using Defense Production Act authority to take equity positions and sign off-take agreements. The MP Materials deal has become the template: $400 million in equity, $150 million in loans, a 10-year off-take commitment, and a price floor on rare earth products. The DOD can increase its stake to 15 percent of the company through warrants.

EXIM Bank launched Project Vault, a $10 billion direct loan facility. It is the largest in the agency’s history, designed to create a strategic minerals stockpile backed by private-sector demand. EXIM has also announced $2.2 billion in additional commitments with Australia.

The U.S. government is now investing at scale. In January 2026, the Development Finance Corporation committed $600 million to the Orion Critical Mineral Consortium, a $1.8 billion platform backed alongside Orion Resource Partners and ADQ, with a stated ambition to scale to roughly $5 billion.

Figure 5: U.S. Government Capital Deployed Toward Critical Minerals, 2025-2026 (Selected Commitments)

| Agency | Commitment | Type | Source |

| EXIM Bank — Project Vault | ~$10.0B | Approved Loan | exim.gov/news/project-vault |

| EXIM Bank — Australia (7 projects) | ~$2.2B | Letters of Interest | exim.gov (Australia LOIs) |

| EXIM Bank — Pakistan (Reko Diq) | ~$1.3B | Announced Financing | U.S. Embassy Pakistan |

| DFC — Orion CMC | ~$0.6B | Closed | dfc.gov (Orion CMC) |

| DFC — Serra Verde, Brazil | ~$0.6B | Signed Loan | dfc.gov (Ministerial PR) |

| DFC — Cove Kaz Capital | ~$0.7B | Announced Financing | dfc.gov (Ministerial PR) |

| DFC — Syrah/Balama + other Africa | ~$0.1B | Equity / Loans | dfc.gov (Syrah) |

| DOD — MP Materials | ~$0.6B | Closed (Equity + Loan) | mpmaterials.com (IR release) |

| DOD — Vulcan / ReElement (OSC) | ~$0.7B | Conditional Loans | war.gov (OSC release) |

| DOD OBBB — National Defense Stockpile | ~$2.0B | Appropriated (P.L. 119-21) | CSIS (OBBB mining analysis) |

| DOD OBBB — Industrial Base Fund (CM) | ~$5.0B | Appropriated (P.L. 119-21) | CSIS (OBBB mining analysis) |

| DOD OBBB — Loan program (direct lending) | ~$0.5B | Appropriated (P.L. 119-21) | CSIS (OBBB mining analysis) |

| DOE — Thacker Pass / Lithium Americas | ~$2.3B | Restructured Loan | THACKER PASS | Department of Energy |

| DOE — CM Processing & Rare Earths FOAs | ~$1.0B | Announced FOAs | energy.gov (CM actions) |

| Commerce — USA Rare Earth (CHIPS) | ~$1.6B | Letter of Intent | investors.usare.com |

| TOTAL (US$ approx.) | ~$29.2B |

Source: Compiled from official agency announcements, 2025-2026.

This is real, and it is meaningful. It is also, by the explicit design of every agency involved, not the answer on its own. The stated goal of EXIM, the DFC, the DOD’s Office of Strategic Capital, and the DOE Loan Programs Office is the same: de-risk the sector enough to crowd in private capital, not replace it.

The constraint is structural. Public capital moves on political timelines. Approval cycles span multiple budget years. Coordination across agencies is uneven. And public balance sheets, even at $29 billion, cannot fund the trillions of dollars in mining and processing capacity the United States will need to build over the next two decades.

The real question is not whether Washington is paying attention. It is whether private capital, in its current form, is structured to match Washington’s ambition.

Why the Structure of Private Capital Matters

One answer is that the United States has the deepest capital markets in the world, and the gap will close on its own once returns become attractive enough. That answer understates the problem.

The pools of private capital available to mining today are not structurally suited to the assets in question. Private equity funds operate on five-to-seven-year clocks and cannot own a 30-year asset. Public mining equities trade on operating earnings and are punished for the capex required to bring new capacity online. Project finance debt pays for construction, but does not share in the upside. Venture capital is the wrong product for any business measured in tonnes per annum.

Royalty and streaming structures, financed off a permanent capital base, fit the asset profile in a way these other vehicles do not. A royalty does not require operational involvement. It scales with production and earns over the entire life of the mine. Held on a balance sheet that does not have to return capital to LPs, a royalty can be owned for as long as the asset keeps producing. The duration of the capital matches the duration of the resource.

The royalty and streaming model has compounded value across precious metals over the past two decades because it is structurally well-fit to long-life mining assets. Wheaton Precious Metals, Franco‑Nevada, Royal Gold, and Triple Flag have created tens of billions of dollars of shareholder value running this model in gold and silver. Critical minerals have, until now, lacked an equivalent platform of scale aligned with U.S. supply chain priorities.

TMCR

I built The Metals Royalty Company to fill that gap.

TMCR began trading on the NASDAQ earlier this year. Our foundational asset is a 2 percent gross overriding royalty on the NORI project, operated by The Metals Company (TMC), one of the largest undeveloped polymetallic resources in the world. NORI-D alone holds 51 million tonnes of probable reserves grading 1.4% nickel, 1.1% copper, 0.13% cobalt, and 31% manganese. The combined net present value across both of TMC’s economic studies is $23.6 billion. Commercial production is targeted for the fourth quarter of 2027, with a ramp to 12 million tonnes per annum of wet nodule production. At steady state, the project is expected to produce approximately 97,000 tonnes of nickel, 70,000 tonnes of copper, 2.4 million tonnes of manganese, and 7,400 tonnes of cobalt per year.

The NORI royalty anchors the platform. The strategy is to acquire and finance royalty and streaming interests across the full spectrum of U.S.-aligned critical minerals: copper, nickel, lithium, uranium, rare earths, antimony, manganese, and the broader basket of materials an industrial economy needs to run on. Tier-1 jurisdictions. Long-life assets. Operators with the capacity to build.

TMCR is structured as a permanent capital vehicle. We do not have a fund clock. We do not need to return capital to LPs. We are aligned with the multi-decade horizons of the projects we finance. Our incentive is to compound capital across cycles, not to maximize an IRR within a fixed window.

What Comes Next

The window for TMCR is open because the need is urgent and the structural alternative does not yet exist at scale. Over the next decade, our intent is to deploy several billion dollars of permanent capital into U.S.-aligned critical minerals royalty and streaming opportunities, partnering with the operators, governments, and policymakers building the next generation of strategic supply.

Rebuilding the industrial base of the United States is generational work. It will take longer than any administration, and it will outlast every fund’s vintage. The capital that gets it done has to be built for the same time horizon as the assets themselves.

That is what we are building.

Disclosure

- This article shall not constitute an offer to sell or the solicitation of an offer to buy any securities. The article does not constitute investment advice. All investments carry risk and each reader is encouraged to consult with his or her individual financial professional. Any action a reader takes as a result of the information presented here is his or her own responsibility. This article is not a solicitation for investment.

- Readers are directed to read and review The Metals Royalty Company Inc. Form F-1 Registration Statement (the “Registration Statement”) under the Securities Act of 1933 filed with the United States Securities and Exchange Commission (“SEC”) and filed on the SEC’s Electronic Data Gathering, Analysis, and Retrieval (EDGAR) system. The foregoing description of The Metals Royalty Company Inc. in this article does not purport to be complete and is qualified in its entirety by reference to the Registration Statement.

This article contains forward-looking information and forward-looking statements within the meaning of applicable securities legislation (collectively, “forward-looking statements”), which reflect management of the Metals Royalty Company Inc.’s (“TMCR”) expectations regarding its future growth, future business plans and opportunities, expected activities, and other statements about future events, results or performances. In certain instances, words such as “predicts”, “projects”, “targets”, “plans”, “expects”, “does not expect”, “budget”, “scheduled”, “estimates”, “forecasts”, “anticipate” or “does not anticipate”, “believe”, “intend” and similar expressions or statements that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved, or the negative or grammatical variation thereof and other variations thereof, or comparable terminology have been used to identify forward-looking statements. These forward-looking statements include, among other things, statements relating to: (a) TMCR’s business plan and strategies; (b) TMCR’s expectations regarding production; (c) services that TMCR intends to offer; and (d) TMCR’s expectations regarding its ability to deliver shareholder value.

Forward-looking statements are not a guarantee of future performance and are based on a number of estimates and assumptions of management, in light of management’s experience and perception of trends, current conditions and expected developments, as well as other factors that management believes to be relevant and reasonable in the circumstances as of the date of this Article, including, without limitation, assumptions regarding: (a) the sources and timing of potential revenue from NORI, as well as the timing and amount of estimated future production related to the NORI Property; (b) the supply and demand for nickel and cobalt (including critical metals and battery cathode feedstocks), steel-making feedstocks, copper and manganese ores; (c) the future prices of such commodities; (d) government regulation of mineral extraction from the deep seafloor and changes in mining laws and regulations; (e) The Metals Royalty Company’s business and future activities; (f) the effect of changes to existing or new legislation, policy or government regulation; (g) TMCR’s goals, strategies and future growth; (h) expectations regarding the performance of the NORI royalty; (i) demand for critical minerals used in EVs and renewable energy storage, which is uncertain; (j) TMCR’s ability to retain key management personnel; (k) projected mining and process recovery rates; (l) other assumptions described in this Article underlying or relating to any forward-looking statements.

Forward-looking statements involve known and unknown risks, as well as uncertainties. These risks may cause TMCR’s actual results, performance or achievements to differ materially from those contemplated, expressed or implied by the forward-looking statements. While TMCR believes that its expectations and estimates reflected in these forward-looking statements are reasonable, there is no guarantee that they will prove to be accurate. A number of factors could cause actual events or results to differ materially from any forward-looking statement, including, without limitation: (a) TMCR is subject to many of the risks faced by The Metals Company Inc. (“TMC”) and our future revenues will be significantly affected by adverse developments related to the NORI property; (b) TMCR does not conduct exploration, development or production efforts and depends on third-party operators for the success of exploration, development or production efforts on projects it acquires royalties on; (c) TMC may not receive the permits and licenses necessary to conduct operations at the NORI property, which would adversely affect TMCR’s expectation of future revenue; (d) TMCR has a limited operating history and thus is subject to risks associated with new business development and there is limited basis on which to evaluate TMCR’s ability to achieve its business objectives; (e) TMCR may not achieve or maintain profitability and positive cash flow; (f) TMCR’s sole royalty interest is not on producing properties and this and any future royalty, streaming or similar interests TMCR acquires, particularly on development stage properties, are subject to the risk that they may never achieve production; (g) TMCR’s sole royalty is subject to buy-back rights that could adversely affect the revenues generated from the asset portfolio; (h) problems concerning the existence, validity, enforceability, terms or geographic extent of our royalty interest on the NORI property could adversely affect TMCR’s business and revenues, and TMCR’s interests may similarly be materially and adversely impacted by a change of control, bankruptcy or the insolvency of operators over which it holds royalties; (i) operators may interpret TMCR’s existing or future royalty or other interests in a manner adverse to TMCR or otherwise may not abide by their contractual obligations; (j) TMCR does not currently generate revenue and will need to raise additional capital to fund operations; (k) TMCR is dependent on favorable government policy for offshore mineral development; (l) the prevailing market price of and demand for nickel, manganese, copper, cobalt and other commodities may have an adverse impact on the value of TMCR’s royalty interests; (m) TMCR’s stock price may be volatile and could decline significantly and rapidly; (n) an active, liquid, and orderly market for TMCR’s common shares may not develop or be sustained; and (o) TMCR’s future growth is to a large extent dependent on TMCR’s ability to acquire additional royalties, streams or similar interests in the future. Additional risks, beyond those summarized below or discussed elsewhere in this Article, may apply to TMCR’s business activities. For additional information with respect to risks, uncertainties and assumptions, see TMCR’s Registration Statement.

TMCR cannot assure readers that actual results will be consistent with the forward-looking statements made in this article and there can be no assurance that such statements will prove to be correct. Accordingly, readers should not place undue reliance on forward-looking statements due to the inherent uncertainties therein.

Except as required by law: (a) The Metals Royalty Company Inc. undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future event or otherwise, after the date on which the statements are made or to reflect the occurrence of unanticipated events, (b) The Metals Royalty Company Inc. does not make, nor do any of its representatives make any representation or warranty, express or implied, as to the accuracy, sufficiency or completeness of the information in this article, (c) neither The Metals Royalty Company Inc. nor any of its representatives shall have any liability whatsoever, under contract, tort, trust or otherwise, to you or any person resulting from the use of the information in this article by you or any of your representatives or for omissions from the information in this article.