For decades, corporate treasuries followed a predictable playbook: Excess cash went into short-term government securities, investment-grade bonds or other highly liquid instruments designed to preserve capital.

But in an era defined by supply chain disruptions, geopolitical tension and the accelerating energy transition, some companies are beginning to rethink what it means to manage risk. Increasingly, the question is not just how to preserve financial capital but how to secure access to the physical materials their businesses depend on.

CFOs and other executives are likely to come under pressure to protect margins and their supply chains within this new environment. In this context, it may not be surprising if corporate treasuries begin holding exposure to critical minerals.

End Of Cheap And Reliable Inputs

For much of the past three decades, companies could assume that raw materials would be available, relatively affordable and sourced through global supply chains that prioritized efficiency.

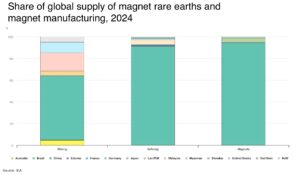

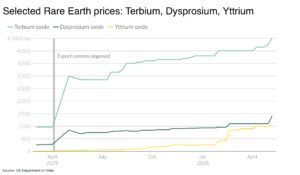

The energy transition alone is dramatically increasing demand for metals such as copper, nickel, lithium and rare earth elements. At the same time, supply growth in many of these materials has been constrained by long permitting timelines, capital shortages in the mining sector and rising geopolitical competition over strategic resources.

The result is a world where commodity availability—and price volatility—can directly impact corporate strategy.

For manufacturers, technology companies and energy developers alike, shortages or price spikes in critical inputs can delay projects, disrupt production schedules and compress margins. Imagine if you are a semiconductor business and rely on gallium, or a magnet business and rely on neodymium—having a treasury could help to protect margins and your business during times of shortage and or price spikes.

Against this backdrop, companies may begin thinking about certain commodities less as operational inputs and more as strategic assets.

From Inventory To Treasury Strategy

Historically, companies have managed commodity risk primarily through procurement strategies or hedging programs using derivatives. But those tools are designed to manage short-term volatility, not long-term structural supply constraints.

Holding strategic exposure to key materials—either physically, financially or through tokenized instruments—could offer a different kind of hedge. For a CFO new to commodities, starting with basic materials that impact their business would make sense.

Consider a large technology manufacturer dependent on copper and rare earth elements, or an energy developer building grid-scale battery systems that require nickel and lithium. If those inputs are expected to become structurally scarce or volatile, maintaining some exposure on the balance sheet could serve as a form of strategic insurance.

In effect, certain commodities could begin to play a role similar to how companies have historically viewed foreign currency reserves or inflation hedges.