Technology companies are still treating rare earth exposure as a downstream risk

For most of the past decade, the technology sector has operated with a blind spot.

In the past, you could build large, valuable businesses without thinking too much about the physical inputs underneath them. For instance, if you were manufacturing semiconductors you didn’t focus on sourcing yttrium. You assumed it would be available. Software scaled and supply chains mostly worked. If something broke, it was usually someone else’s problem. Now that era is ending and companies need to focus on their supply chains upstream, in some cases all the way to actual mining operations for their most critical inputs.

For companies utilizing rare earth elements, understanding the supply chain risks associated with their sourcing is a good place to start derisking commodity exposure upstream. Despite the name, these elements are not particularly rare, but their processing is largely controlled by China. Thus, in some cases, they are difficult to obtain or have huge price volatility. I’m talking about a group of 17 elements—neodymium, praseodymium, dysprosium, terbium, among others—that tend to occur together in the earth’s crust. What makes rare earth elements important is what they enable.

For instance, rare earth magnets—built from these elements—are critical to electric vehicles, wind turbines, robotics, and a growing range of data center and advanced electronics systems. If you’re building anything tied to electrification (AI infrastructure or automation) you are already exposed to the rare earth supply chain. And that supply chain is starting to tighten.

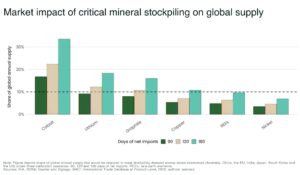

THE SUPPLY CHAIN CREATED A CHOKEPOINT

For most technology companies, rare earth exposure feels indirect. You’re not buying oxides or metals—you’re buying components like motors, systems, and equipment. But that abstraction hides a very real risk. Many of these products rely heavily on rare earths and disruptions in this market, whether price spikes or shortages, can have a real impact on product availability and/or price.

A significant portion of the global rare earth supply chain—particularly processing and refining—runs through China. Today, roughly 85–90% of rare earth processing capacity is concentrated there.

Even when rare earth elements are mined in other countries, they are often shipped to China for separation before re-entering global markets. That model worked for years until it created a chokepoint.

There wasn’t a sudden rare earth shortage. The problem was more subtle, and more disruptive: tighter supply, pricing volatility, and less predictable access.

For companies operating on compressed timelines, that matters.